Volatility & Derivatives

In this post we give an introduction to the Heston model which is one of the most used stochastic volatility model. It assumes that the

In a previous article (see Options, Greeks and P&L Decomposition (Part 1)) we analysed the decomposition of the P&L of an option strategy in a short period of time with the major first and second order greeks.

In this new article, we assume that the option is kept for a certain period of time, delta-hedged regularly, and we study the P&L of the strategy in theory and in practice through simulations.

We show that under certain assumptions, the P&L of a delta-hedged option is mostly explained by the gamma / theta P&L when the option is kept until expiry, it is not depending on the path of the implied volatility.

The Python code used in simulations is available at the end of the article.

We consider a delta-hedged option strategy consisting on:

We assume that there are no transaction costs, the risk-free interest rate and the dividend yield are constant equal to r and q respectively.

The P&L of the strategy between t and t + δt is equal to:

Equation 1

P = P(t, S, σ) is the Black-Scholes price of the option.

With a Taylor expansion of the option price we have:

Equation 2

with Δ: delta, Γ: gamma, Θ: theta, v: vega of the option.

And P is solution of the Black-Scholes equation, so we have the following relationship between the theta (Θ) and the gamma (Γ) of the option:

Equation 3

Replacing Θ in Equation 2 with its expression from Equation 3 and δP in Equation 1 with its expression from Equation 2 we get the following expression for the P&L of the strategy between t and t + δt:

Equation 4

with σr the realised volatility:

So if we neglect other higher order greeks such as vanna, volga, charm and so on, the P&L of the strategy between t and t + δt is mostly explained by

If we maintain the strategy for a certain time, with a regular delta-hedging, the P&L of the strategy will be path-dependent, the gamma and the vega of the option with change with the moneyness of the option, its time to maturity or the implied volatility.

Going back to Equation 1, if we neglect interest rates and dividends and we assume that we delta-hedge the option regularly using the implied volatility at inception, the P&L between t0 and t1 is:

Equation 6

If we consider a European vanilla option such as a call option and we assume that the option is kept until expiry, we see that the P&L of the strategy is no more depending on the implied volatility path. The price of the option at expiry T is its final payoff (ST – K)+ with K the strike price of the option, and the P&L becomes:

Equation 7

If the option is delta-hedged with a high enough frequency, the P&L at expiry of the delta-hedged option is actually very close to the gamma / theta P&L by integrating Equation 4 without the vega term and the residual.

Equation 8

Let’s test it through simulations.

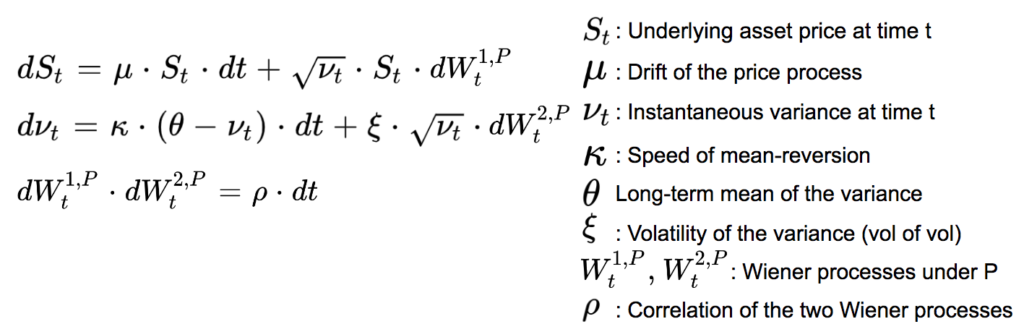

We assume that the stock price follows a Heston model.

Both the stock price and its volatility are stochastic. Under the real probability P we have:

The Heston Model

Equation 8

We use the following Euler discretization for the simulations, using the full truncation method scheme replacing nu by the maximum between 0 and nu in the mean reversion term, in the square root of the variance and in the asset price expression:

Equation 9

References: Roger Lord, Remmert Koekkoek, Dick van Dijk (2008) “A comparison of biased simulation schemes for stochastic volatility models”

N1 and N2 are independent random variable, they follow a standard normal distribution.

In order to simulate the implied volatility, we assume that the implied variance (the square of the implied volatility) is equal to the instantaneous variance plus a certain variance premium p:

Equation 10

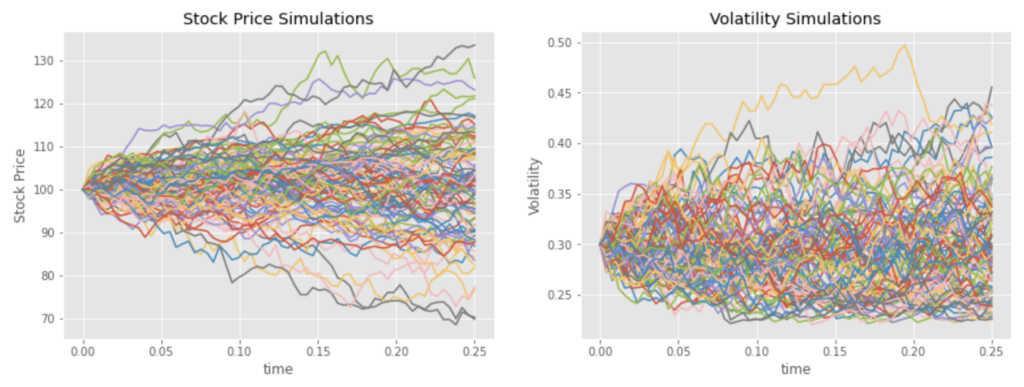

We use the following parameters and run 100 simulations:

S0 = 100, ν0 = 0.22, μ = 5%, κ = 5, θ = 0.22, ξ = 0.5, ρ = -50%, p = 0.32 – 0.22

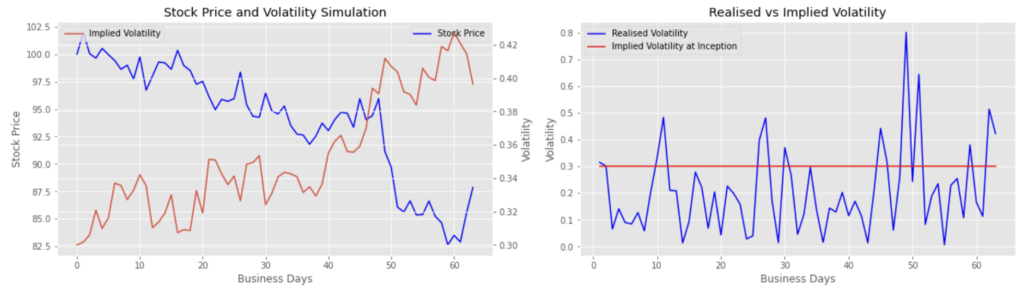

And we consider the two following simulations with a 3-month horizon:

Simulation 1: stock price up / vol down

Simulation 2: stock price down / vol up

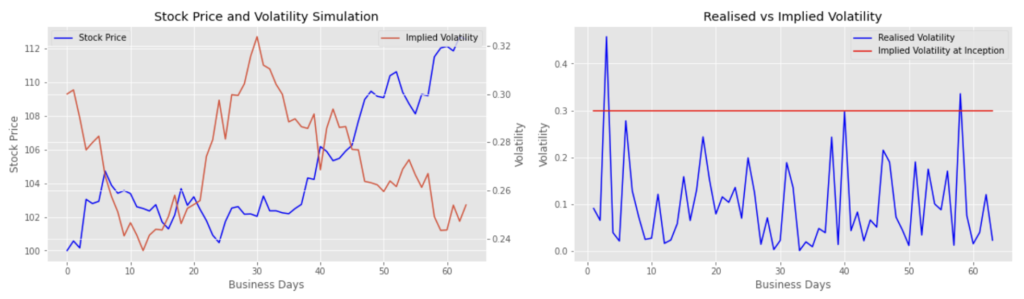

We consider a 3-month call option with a strike price at 105, and we price the option with the Black-Scholes formula assuming the risk-free interest rate r = 3% and the dividend yield q = 0%.

The strategy consists on the purchase of the option, it is delta-hedged on a daily basis using the volatility at inception until the maturity of the option.

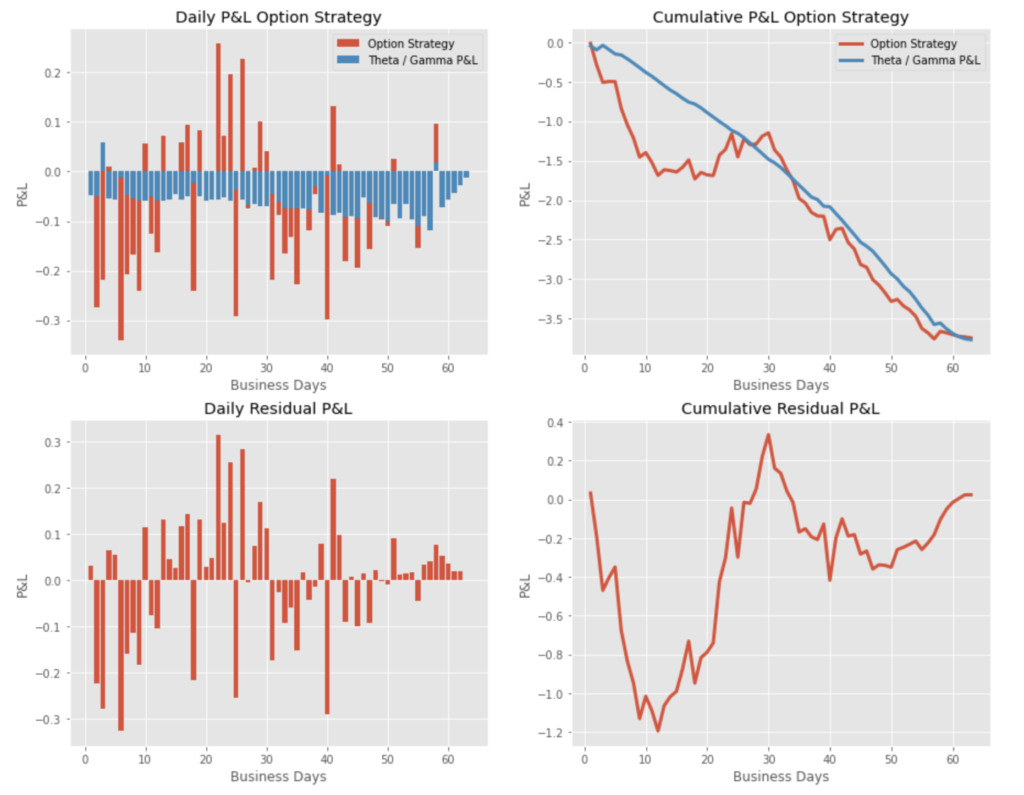

As highlighted below, in Simulation 1 (stock price up / vol down) , the P&L of the strategy is negative at maturity. The realised volatility (see above) is most of the time below the implied volatility, and the gamma / theta P&L has a negative contribution. At maturity, most of the P&L is explained by the Theta / Gamma P&L, the cumulative residual P&L, mostly explained by the Vega P&L, is close to zero at the maturity of the option.

P&L Option Strategy – Simulation 1

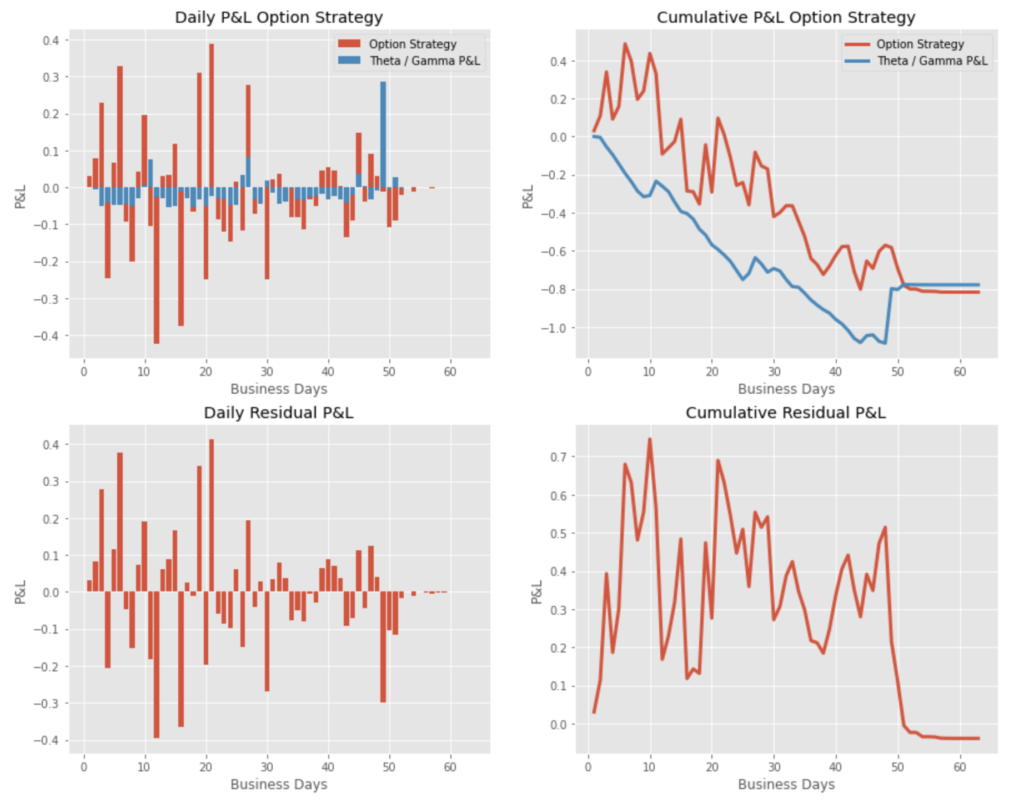

In Simulation 2 (stock price down, vol up), the P&L is a bit less negative. The realized volatility is a bit less below the implied volatility at inception (see above). Again, most of the P&L at maturity is explained by the Theta / Gamma P&L, the cumulative residual P&L converging to a value close to zero.

P&L Option Strategy – Simulation 2

In both cases, the P&L is no more directional, as the option is delta-hedged.

Even if the volatility P&L (vega, vanna, volga, …) can have important impact on the daily P&L, when the option is kept until expiry, it cancels out cumulatively and the final P&L is mostly explained by the gamma / theta P&L.

Save 25% on All Quant Next Courses with the Coupon Code: QuantNextBlog25

For students and graduates: We offer a 50% discount on all courses, please contact us if you are interested: contact@quant-next.com

We summarize below quantitative finance training courses proposed by Quant Next. Courses are 100% digital, they are composed of many videos, quizzes, applications and tutorials in Python.

Complete training program:

Options, Pricing, and Risk Management Part I: introduction to derivatives, arbitrage free pricing, Black-Scholes model, option Greeks and risk management.

Options, Pricing, and Risk Management Part II: numerical methods for option pricing (Monte Carlo simulations, finite difference methods), replication and risk management of exotic options.

Options, Pricing, and Risk Management Part III: modelling of the volatility surface, parametric models with a focus on the SVI model, and stochastic volatility models with a focus on the Heston and the SABR models.

A la carte:

Monte Carlo Simulations for Option Pricing: introduction to Monte Carlo simulations, applications to price options, methods to accelerate computation speed (quasi-Monte Carlo, variance reduction, code optimisation).

Finite Difference Methods for Option Pricing: numerical solving of the Black-Scholes equation, focus on the three main methods: explicit, implicit and Crank-Nicolson.

Replication and Risk Management of Exotic Options: dynamic and static replication methods of exotic options with several concrete examples.

Volatility Surface Parameterization: the SVI Model: introduction on the modelling of the volatility surface implied by option prices, focus on the parametric methods, and particularly on the Stochastic Volatility Inspired (SVI) model and some of its extensions.

The SABR Model: deep dive on on the SABR (Stochastic Alpha Beta Rho) model, one popular stochastic volatility model developed to model the dynamic of the forward price and to price options.

The Heston Model for Option Pricing: deep dive on the Heston model, one of the most popular stochastic volatility model for the pricing of options.

First we import the libraries that will be used and we create a class EuropeanOptionBS with Black-Scholes prices and Greeks with closed-form formulas.

Import Libraries:

import matplotlib.pyplot as plt

plt.style.use('ggplot')

import math

import numpy as np

import pandas as pd

from scipy.stats import norm

%matplotlib inlineBlack-Scholes formula and greeks:

class EuropeanOptionBS:

def __init__(self, S, K, T, r, q, sigma, Type):

self.S = S

self.K = K

self.T = T

self.r = r

self.q = q

self.sigma = sigma

self.Type = Type

self.d1 = self.d1()

self.d2 = self.d2()

self.price = self.price()

self.delta = self.delta()

self.theta = self.theta()

self.vega = self.vega()

self.gamma = self.gamma()

self.volga = self.volga()

self.vanna = self.vanna()

def d1(self):

d1 = (math.log(self.S / self.K) \

+ (self.r - self.q + .5 * (self.sigma ** 2)) * self.T) \

/ (self.sigma * self.T **.5)

return d1

def d2(self):

d2 = self.d1 - self.sigma * self.T **.5

return d2

def price(self):

if self.Type == "Call":

price = self.S * math.exp(-self.q * self.T) * norm.cdf(self.d1) \

- self.K * math.exp(-self.r * self.T) * norm.cdf(self.d2)

if self.Type == "Put":

price = self.K * math.exp(-self.r* self.T) * norm.cdf(-self.d2) \

- self.S * math.exp(-self.q * self.T) * norm.cdf(-self.d1)

return price

def delta(self):

if self.Type == "Call":

delta = math.exp(-self.q * self.T) * norm.cdf(self.d1)

if self.Type == "Put":

delta = -math.exp(-self.q * self.T) * norm.cdf(-self.d1)

return delta

def theta(self):

if self.Type == "Call":

theta1 = -math.exp(-self.q * self.T) * \

(self.S * norm.pdf(self.d1) * self.sigma) / (2 * self.T**.5)

theta2 = self.q * self.S * math.exp(-self.q * self.T) * norm.cdf(self.d1)

theta3 = -self.r * self.K * math.exp(-self.r * self.T) * norm.cdf(self.d2)

theta = theta1 + theta2 + theta3

if self.Type == "Put":

theta1 = -math.exp(-self.q * self.T) * \

(self.S * norm.pdf(self.d1) * self.sigma) / (2 * self.T **.5)

theta2 = -self.q * self.S * math.exp(-self.q * self.T) * norm.cdf(-self.d1)

theta3 = self.r * self.K * math.exp(-self.r * self.T) * norm.cdf(-self.d2)

theta = theta1 + theta2 + theta3

return theta

def vega(self):

vega = self.S * math.exp(-self.q * self.T) * self.T**.5 * norm.pdf(self.d1)

return vega

def gamma(self):

gamma = math.exp(-self.q * self.T) * norm.pdf(self.d1) / (self.S * self.sigma * self.T**.5)

return gamma

def volga(self):

volga = self.vega / self.sigma * self.d1 * self.d2

return volga

def vanna(self):

vanna = -self.vega / (self.S * self.sigma * self.T**.5) * self.d2

return vannaSimulation of stock price and implied volatility with Heston model using full truncature scheme:

def simulate_market(S0, T, mu, kappa, nu0, theta, xi, rho, var_premium, N, nstep):

np.random.seed(5)

dW1 = np.random.normal(size = (N, nstep))

dW2 = rho * dW1 + np.sqrt(1 - rho**2) * np.random.normal(size = (N, nstep))

dt = T / nstep

S = np.empty((N, nstep + 1))

v = np.empty((N, nstep + 1))

vplus = np.empty((N, nstep + 1))

S[:, 0] = S0

v[:, 0] = nu0

vplus[:, 0] = nu0

for t in range(1, nstep + 1):

S[:, t] = S[:, t - 1] * np.exp((mu - .5 * vplus[:, t - 1]) * dt + np.sqrt((vplus[:, t - 1]) * dt) * dW1[:, t - 1])

v[:, t] = v[:, t - 1] + kappa * (theta - vplus[:, t - 1]) * dt + xi * np.sqrt(vplus[:, t - 1] * dt) * dW2[:, t - 1]

vplus[:, t] = [max(0., v[i, t]) for i in range(N)]

v = v + var_premium

return S, v#parameters:

S0 = 100

T = 63 / 252 #maturity

mu = .05

kappa = 5.0

nu0 = .2**2

theta = .2***2

xi = .5

rho = -.5

var_premium = .3**2 - .2**2

N = 100

nstep = 63

simu = simulate_market(S0, T, mu, kappa, nu0, theta, xi, rho, var_premium, N, nstep)

time = np.arange(0, T + T / nstep, T / nstep)#plot simulations

fig, axs = plt.subplots(1, 2, figsize = (15, 5))

for i in range(N):

axs[0].plot(time, simu[0][i])

axs[1].plot(time, np.sqrt(simu[1][i]))

axs[0].set_title('Stock Price Simulations')

axs[0].set_xlabel('time')

axs[0].set_ylabel('Stock Price')

axs[1].set_title('Volatility Simulations')

axs[1].set_xlabel('time')

axs[1].set_ylabel('Volatility')

plt.show();#Simulation 1 (for simulation 2 uses the 22th simulation paths)

StockPrice = simu[0][0] #simu[0][22]

ImpliedVol = np.sqrt(simu[1][0]) #np.sqrt(simu[1][22])

RealisedVol = [np.sqrt((StockPrice[i + 1] / StockPrice[i] - 1)**2 * 252) for i in range(nstep)]

fig, axs = plt.subplots(1, 2, figsize = (20, 5))

ax2 = axs[0].twinx()

axs[0].set_title('Stock Price and Volatility Simulation')

axs[0].set_xlabel('Business Days')

axs[0].plot(range(0, nstep + 1), StockPrice, color = 'b')

ax2.plot(range(0, nstep + 1), ImpliedVol)

axs[0].set_ylabel('Stock Price')

ax2.set_ylabel('Volatility')

axs[0].legend(['Stock Price'])

ax2.legend(['Implied Volatility'])

axs[1].set_title('Realised vs Implied Volatility')

axs[1].set_xlabel('Business Days')

axs[1].plot(range(1, nstep + 1), RealisedVol, color = 'b')

axs[1].set_ylabel('Volatility')

axs[1].plot(range(1, nstep + 1), [ImpliedVol[0] for i in range(1, nstep + 1)], color = 'r')

axs[1].legend(['Realised Volatility', 'Implied Volatility at Inception'])

plt.show()P&L Simulations

#option parameters

K = 105 # strike price

r = .03 # risk-free interest rate

q = .0 # dividend

Type = "Call"#Simulation 1 (for simulation 2 uses the 22th simulation paths)

StockPrice = simu[0][0] #simu[0][22]

ImpliedVol = np.sqrt(simu[1][0]) #np.sqrt(simu[1][22])

OptionPrice = [EuropeanOptionBS(StockPrice[i], K, T - time[i], r , q, ImpliedVol[i], Type).price for i in range(nstep)]

OptionDelta = [EuropeanOptionBS(StockPrice[i], K, T - time[i], r , q, ImpliedVol[0], Type).delta for i in range(nstep)]

OptionVega = [EuropeanOptionBS(StockPrice[i], K, T - time[i], r , q, ImpliedVol[0], Type).vega for i in range(nstep)]

OptionGamma = [EuropeanOptionBS(StockPrice[i], K, T - time[i], r , q, ImpliedVol[0], Type).gamma for i in range(nstep)]

OptionTheta = [EuropeanOptionBS(StockPrice[i], K, T - time[i], r , q, ImpliedVol[0], Type).theta for i in range(nstep)]

OptionPrice.append(max(StockPrice[nstep] - K, 0)) #final payoff

#no Delta-Hedge

DailyPandL_noDH = [OptionPrice[i + 1] - OptionPrice[i] for i in range(nstep)]

CumPandL_noDH = [OptionPrice[i + 1] - OptionPrice[0] for i in range(nstep)]

#with Delta-Hedge

DailyPandL_DH = [DailyPandL_noDH[i] - OptionDelta[i] * (StockPrice[i + 1] - StockPrice[i]) for i in range(nstep)]

CumPandL_DH = np.cumsum(DailyPandL_DH)

#Vega P&L

DailyVegaPandL = [OptionVega[i] * (ImpliedVol[i + 1] - ImpliedVol[i]) for i in range(nstep)]

CumVegaPandL = np.cumsum(DailyVegaPandL)

#Gamma P&L

DailyGammaPandL = [.5 * OptionGamma[i] * (StockPrice[i + 1] - StockPrice[i])**2 for i in range(nstep)]

CumGammaPandL = np.cumsum(DailyGammaPandL)

#Theta P&L

DailyThetaPandL = [OptionTheta[i] * (time[i + 1] - time[i]) for i in range(nstep)]

CumThetaPandL = np.cumsum(DailyThetaPandL)

#Theta + Gamma P&L

DailyThetaGammaPandL = [DailyGammaPandL[i] + DailyThetaPandL[i] for i in range(nstep)]

CumThetaGammaPandL = [CumGammaPandL[i] + CumThetaPandL[i] for i in range(nstep)]

fig, axs = plt.subplots(2, 2, figsize = (15, 12))

axs[0][0].bar(range(1, nstep + 1), DailyPandL_DH)

axs[0][0].bar(range(1, nstep + 1), DailyThetaGammaPandL)

axs[0][0].set_xlabel('Business Days')

axs[0][0].set_ylabel('P&L')

axs[0][0].set_title('Daily P&L Option Strategy')

axs[0][0].legend(['Option Strategy', 'Theta / Gamma P&L'])

axs[0][1].plot(range(1, nstep + 1), CumPandL_DH, linewidth = 3)

axs[0][1].plot(range(1, nstep + 1), CumThetaGammaPandL, linewidth = 3)

axs[0][1].set_xlabel('Business Days')

axs[0][1].set_ylabel('P&L')

axs[0][1].set_title('Cumulative P&L Option Strategy')

axs[0][1].legend(['Option Strategy', 'Theta / Gamma P&L'])

axs[1][0].bar(range(1, nstep + 1), np.array(DailyPandL_DH) - np.array(DailyThetaGammaPandL))

axs[1][0].set_xlabel('Business Days')

axs[1][0].set_ylabel('P&L')

axs[1][0].set_title('Daily Residual P&L')

axs[1][1].plot(range(1, nstep + 1), np.array(CumPandL_DH) - np.array(CumThetaGammaPandL), linewidth = 3)

axs[1][1].set_xlabel('Business Days')

axs[1][1].set_ylabel('P&L')

axs[1][1].set_title('Cumulative Residual P&L')

plt.show();In this post we give an introduction to the Heston model which is one of the most used stochastic volatility model. It assumes that the

In the previous post (link) dedicated to the pricing of defaultable bonds with a reduced form model, we saw how to price a zero coupon

The Merton Jump Diffusion (MJD) model was introduced in a previous article (link). It is an extension of the Black-Scholes model adding a jump part