![C(S_t,t)=e^{-r*(T-t)}*[S_t*e^{r*(T-t)}*N(d_1)-K*N(d_2)]](https://lh7-us.googleusercontent.com/ZikLA8_p7CSVdthiPhOlFTpjUin3FytodeiPt6Qad0uQvqDJZqg4m6JwaADEni5h4DuWnf2ZLSmwiSengJPeY4yftvvHAFTepIDHVcuWYphHuZyIOcszYMh3vF4aFnzxiNHjRW4IcXZvDJT0NVwLp2A2nQ=s2048)

Volatility & Derivatives

In this post we give an introduction to the Heston model which is one of the most used stochastic volatility model. It assumes that the

The Black-Scholes model is a pricing model used to determine the theoretical price of options contracts. It was developed by Fischer Black and Myron Scholes in 1973 and later refined by Robert Merton.

The model assumes that the financial market has two assets, one risky asset such as a stock price and one risk-free asset such as a bank account.

The risky asset S follows a Geometric Brownian motion, with the following stochastic differential equation:

Wt is a Wiener process, μ is the drift and σ the volatility of the stock price.

The initial model also assumed that:

Under these assumptions, Black and Scholes showed that the price of a European option on the underlying asset S with the final payoff g(S) is a solution of Black Scholes partial differential equation (PDE):

You will find the demonstration in this article: The Black-Scholes Model.

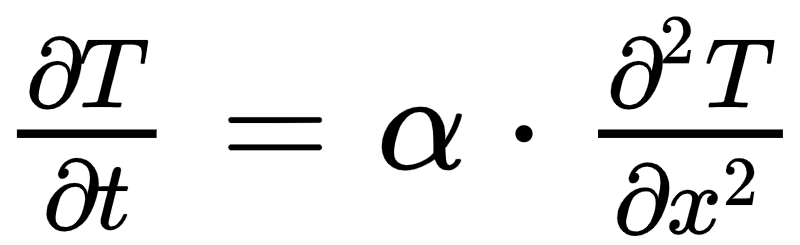

The heat equation describes how heat diffuses through a given region over time.

The heat equation is a fundamental partial differential equation that describes how heat diffuses through a given region over time. It was introduced by Joseph Fourier in 1807.

In one spatial dimension, it can be expressed as:

Where T(x, t) is the temperature at position x and time t, and α is the thermal diffusivity of the material which quantifies the rate of heat transfer from warm environment to cold environment.

Both the Black-Scholes and the heat equations are diffusion equations, of the option price for the former one, of temperature for the latter one.

Both equations have in common to have a relationship between the first order derivative with respect to time and up to a second order derivative with respect to space, if we consider S as the spatial equivalent.

The transfer of heat from warm environnement to cold environment is in a way equivalent to the erosion of option price due to the passage of time, or time decay.

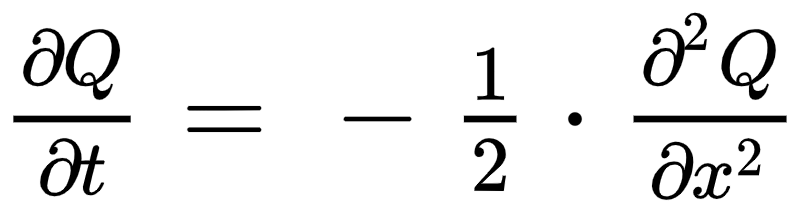

If we assume that the interest rate r is equal to zero we obtain the following relationship between the first order derivative with respect to time and the second order derivative of the option price with respect to the asset price from the Black-Scholes equation.

The time decay (the theta) on the left side is related to the convexity of the option, which is controlled by the second order derivative of the option price with respect to the asset price (the gamma), and uncertainty with the volatility of the asset price.

This relationship is very similar to the heat equation.

Actually, with some changes of variables, we can transform the Black Scholes PDE into a standard heat equation.

With

We have

and

So we get

with the terminal condition

The solution of the heat equation is given by the following integral:

It is not always possible to simplify the integral, it depends on the expression of g.

For call options

and we obtain the Black-Scholes formula by integration:

Similarly for put options

Save 25% on All Quant Next Courses with the Coupon Code: QuantNextBlog25

For students and graduates: We offer a 50% discount on all courses, please contact us if you are interested: contact@quant-next.com

We summarize below quantitative finance training courses proposed by Quant Next. Courses are 100% digital, they are composed of many videos, quizzes, applications and tutorials in Python.

Complete training program:

Options, Pricing, and Risk Management Part I: introduction to derivatives, arbitrage free pricing, Black-Scholes model, option Greeks and risk management.

Options, Pricing, and Risk Management Part II: numerical methods for option pricing (Monte Carlo simulations, finite difference methods), replication and risk management of exotic options.

Options, Pricing, and Risk Management Part III: modelling of the volatility surface, parametric models with a focus on the SVI model, and stochastic volatility models with a focus on the Heston and the SABR models.

A la carte:

Monte Carlo Simulations for Option Pricing: introduction to Monte Carlo simulations, applications to price options, methods to accelerate computation speed (quasi-Monte Carlo, variance reduction, code optimisation).

Finite Difference Methods for Option Pricing: numerical solving of the Black-Scholes equation, focus on the three main methods: explicit, implicit and Crank-Nicolson.

Replication and Risk Management of Exotic Options: dynamic and static replication methods of exotic options with several concrete examples.

Volatility Surface Parameterization: the SVI Model: introduction on the modelling of the volatility surface implied by option prices, focus on the parametric methods, and particularly on the Stochastic Volatility Inspired (SVI) model and some of its extensions.

The SABR Model: deep dive on on the SABR (Stochastic Alpha Beta Rho) model, one popular stochastic volatility model developed to model the dynamic of the forward price and to price options.

The Heston Model for Option Pricing: deep dive on the Heston model, one of the most popular stochastic volatility model for the pricing of options.

In this post we give an introduction to the Heston model which is one of the most used stochastic volatility model. It assumes that the

In the previous post (link) dedicated to the pricing of defaultable bonds with a reduced form model, we saw how to price a zero coupon

The Merton Jump Diffusion (MJD) model was introduced in a previous article (link). It is an extension of the Black-Scholes model adding a jump part